The two words that explain why the Fed might tank the economy

It's Halloween and Jerome Powell is afraid of "unanchored expectations."

The aggressive campaign of interest rate hikes that the Federal Reserve launched back in March has had a big impact on the U.S. economy. The S&P 500 has fallen almost 20 percent since its January peak, and a growing number of economists fear that the country is headed for a recession.

These rate hikes are meant to bring down inflation, which is still near 40-year highs. But the Fed is also trying to influence the public’s expectations for future inflation. Fed Chairman Jerome Powell laid out his reasoning in a gloomy Aug. 26th address at the Jackson Hole Economic Symposium.

“We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored,” Powell said.

That last bit about keeping inflation expectations anchored is critical for understanding the forcefulness of the Fed’s response. Several economists told me that if people start to expect inflation to remain high, they could change their behavior in ways that make that expectation a self-fulfilling prophecy.

“If you expect inflation going up and going forward, and you want to purchase a car or large durable good, you’d do it before prices increase,” said Georgetown University economist Francesco D'Acunto. That, he said, “will push prices even further up.”

Workers might push for bigger raises if they expect the cost of living to rise in the coming year. And businesses might preemptively raise their prices if they expect wages and the cost of raw materials to increase.

If feedback loops like these get established, it will become much harder to drive inflation back down to the Fed’s 2 percent target.

So some economists think it’s almost impossible for the Fed to be too hawkish right now. If people believe that the Fed will do whatever it takes to get inflation down—including making unemployment rise—that will shift public expectations in a way that actually helps keep inflation down. Paradoxically, that could reduce the amount of tightening the Fed ultimately needs to do, and spare us additional economic pain.

But some inflation doves disagree. While most acknowledge that unanchored expectations could in theory become a problem, they see little to no evidence that it’s an actual problem right now. The far greater risk, in their view, is that the Fed tightens too rapidly and triggers an unnecessary recession.

One prominent dove is Claudia Sahm, an economist who spent 12 years working at the Fed. “An obsession with inflation expectations will destroy the global economy and the first job-full recovery in decades,” she tweeted earlier this month.

In a phone interview, Sahm told me that the Fed has “no data that says inflation expectations are deanchoring, and yet they are going to tank the global economy.”

With the global economy tottering on the edge of recession, an ongoing war against Ukraine (that’s helping fuel an energy crisis in Europe), and a declining yet latent pandemic, the stakes over how fast the Fed moves are high. If doves like Sahm are right, then it might make sense for the Fed to pause its rate-hiking campaign and see what happens to inflation over the next few months. But right now, the leadership of the Fed thinks she’s wrong. They believe aggressive action today will avoid the need for an even more painful round of monetary tightening down the road.

The danger of unanchored expectations

Most economists believe that if inflation expectations were to become unanchored, inflation would get much worse. Economists’ thinking on this question is deeply influenced by the high inflation of the 1970s.

During that decade, workers started to ask for larger raises to cover the higher prices they expected over the following year. That led to more money circulating through the economy, encouraging businesses to raise their prices.

The person who finally ended this wage-price spiral was Paul Volcker, who became Fed chair in 1979. Volcker made clear that fighting inflation was his top priority and that he would push short-term interest rates as high as necessary to get inflation under control. They went very high indeed, reaching a peak of more than 19 percent in 1981. The result was a pair of severe recessions that started in 1980 and 1981, respectively. Unemployment peaked at nearly 11 percent in 1982.

One reason the “Volcker disinflation was so costly,” according to Carola Binder, an economist at Haverford College, was that “no one really believed the Fed was committed” to cutting inflation. As a result, “expectations didn’t come down very easily.”

The belief that unanchored expectations were to blame for the pain of the 1970s is shared by many in conventional macroeconomic circles, and, most importantly, within the Federal Reserve. In a speech earlier this month, New York Fed President John Williams argued, “Anchoring of longer-term expectations is critical to keeping high inflation from becoming embedded in the psychology of consumers and businesses, which we know from the past is costly to undo.”

Even doves acknowledge that unanchored expectations would be catastrophic. Sahm told me that “an inflationary mentality, if it were to set in, would make it much harder to bring inflation down.”

Inflation expectations are well anchored—at least for now

Most economists across the political spectrum also agree that inflation expectations have not become unanchored—at least not yet. Most consumers and financial market participants expect future inflation to be roughly in line with the Fed’s 2 percent target over the next few years.

Let’s look at two important sources of data.

One is the University of Michigan Survey of Consumers. Every month, researchers ask a random sample of American consumers what they expect the inflation rate to be over the next five years.

The other is a market forecast called the five-year inflation breakeven. This is based on the price of Treasury Inflation Protected Securities, a special kind of government bond whose principal is automatically adjusted for inflation. Comparing the price of ordinary five-year Treasury bonds with five-year TIPS reveals how much inflation bond market participants expect over the next five years.

As you can see, neither measure of inflation expectations is very far above the Fed’s 2 percent target.

The fundamental disagreement is about why expectations have remained anchored in recent months.

Hawks believe it’s precisely because the Fed has bolstered its credibility with hawkish policies. As demonstrated in the chart above, five-year inflation expectations drifted just over 3 percent early this year, at a time when the Fed was signaling that it would raise rates gradually—by no more than 0.25 percent at each meeting. But then the 5-year TIPS spread fell rapidly in May and June 2022, as the Fed accelerated its rate hiking campaign and Jerome Powell’s anti-inflation rhetoric became increasingly emphatic.

So although hawkish economists are happy to see anchored expectations, they do not take them as a sign that the Fed should ease its rate hikes. In fact, they feel the opposite. Larry Summers, for example, has said that since low expectations may reflect a belief in Powell’s hawkishness, easing off now would risk unanchoring.

These economists recognize that further rate hikes will cause substantial economic pain, with U.S. unemployment rising perhaps as high as 7 percent or 8 percent. But in their eyes, this economic pain may be worth it. They argue that it was precisely a lack of inflation-fighting resolve during the 1970s that led to unemployment levels above 10 percent in 1981.

“Extremely shaky foundations?”

Doves see things differently. For them, the inflation of the last year mainly reflects a string of unlucky breaks: COVID-related supply disruptions followed by the Russian invasion of Ukraine. They predict that once those shocks are in the rearview mirror, the U.S. will naturally return to the low-inflation status quo of the 2010s, which is why they aren’t surprised that the public expects inflation to return to normal levels.

In 2021, Jeremy Rudd, an economist at the Federal Reserve, published a bombshell paper arguing that since the 1960s, economists have been overly worried about inflation expectations. He argued that their fear “rests on extremely shaky foundations” and that the empirical evidence for it “was never very strong.” Many left-wing economists share his belief that conventional economics places too much weight on inflation expectations, especially right now.

After all, the Fed’s current hiking schedule is unprecedentedly quick. And monetary policy has long and variable lags, meaning that the Fed can’t be sure exactly how or when its interest rates will affect the economy.

To steal a metaphor from Larry Summers: Imagine you’re taking a shower at a hotel. You don’t know how far to turn the dial to get the Goldilocks temperature, and it takes a few seconds for a change in the dial to affect the water temperature. Powell is effectively turning the dial all the way to scalding without stopping to check the water temperature along the way.

Nathan Tankus, a left-leaning economics blogger, argues that there is “basically no empirical macroeconomic support” for this kind of approach. The costs of Fed action, though, are certain to be harsh, as millions of workers may be forced out of a job by a Fed-induced recession.

Both Tankus and Sahm described the Fed’s reliance on the 1970s as “zombie” economics that used outdated ideas of inflation expectations to justify an overly harsh response in the present. They point to two considerable ways today’s economy differs from that of the 1970s.

First, Sahm told me that a wage-price spiral—when workers demand raises in anticipation of higher prices—was a much bigger concern in the 1970s when the economy was highly unionized. Unionized workers had more leverage to ask for higher wages. Today’s more vulnerable workforce may want raises, but they have less power to secure them.

Moreover, Sahm pointed out that wages have actually been rising more slowly than inflation over the past year, which casts doubt on the theory that wage growth has been a major driver of inflation.

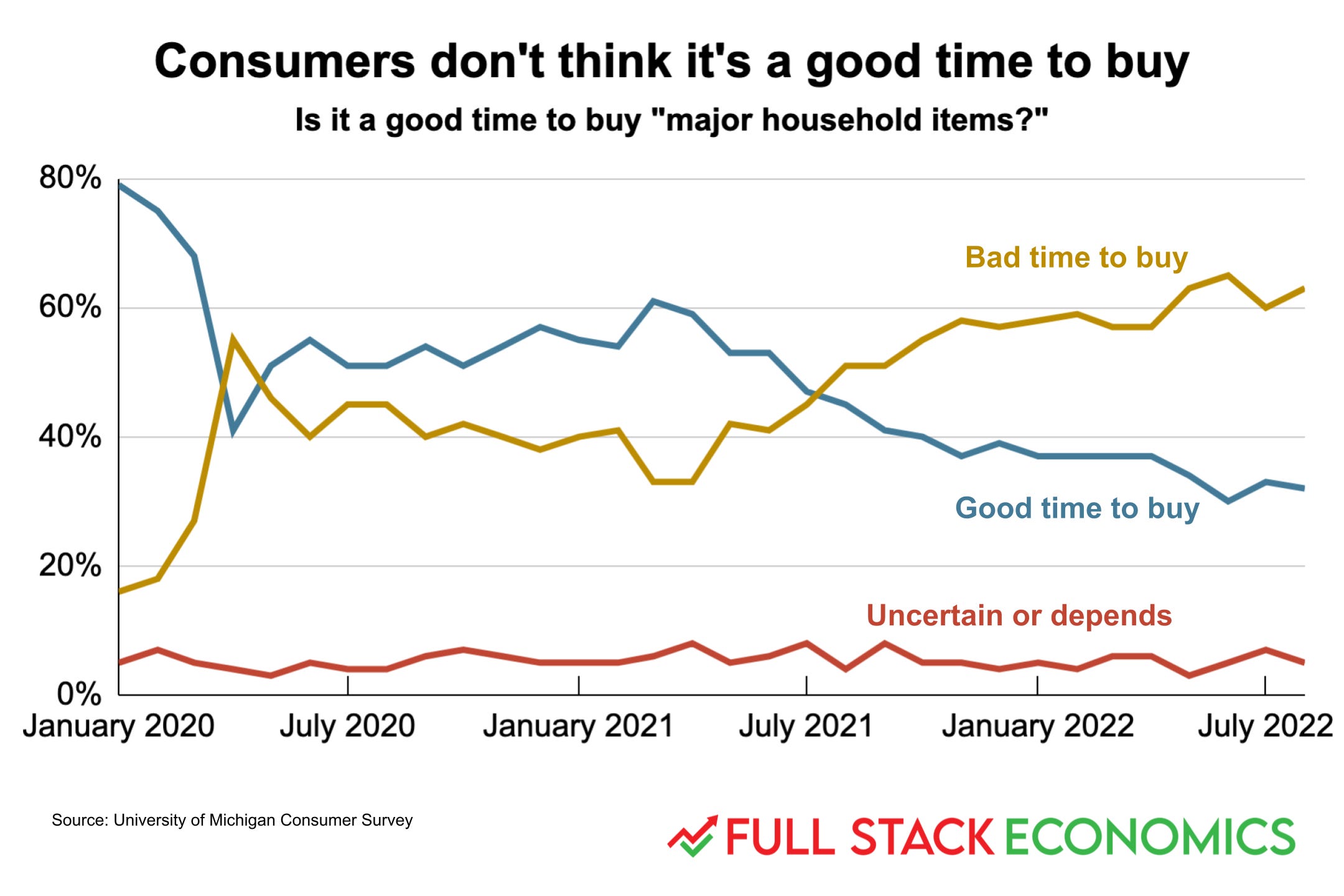

Sahm also argued there’s no evidence consumers are rushing to buy goods before inflation goes up. Quite the contrary.

Sahm points to an item in the Michigan survey: “Do you think now is a good or a bad time for people to buy major household items?” Right now, “the majority of people are saying it’s a bad time to buy because prices are high,” Sahm told me. That’s the opposite of what you’d expect to see if consumer expectations were driving inflation higher.

Tankus’ and Sahm’s points about inflation expectations currently being anchored do not necessarily contradict the hawks’ view that inflation expectations are anchored because the Fed has been so contractionary. It’s possible that if the Fed had not, to this point, pursued such strict tightening, inflation expectations would currently be rising and we’d be seeing a wage-price spiral. But nobody knows for sure. And in the absence of certainty, Powell will keep that shower handle turned all the way to hot.

Aden Barton is an economics student at Harvard. You can follow him on Twitter.

Two words to explain how insane this article as well as FED policy, you're wrongheaded.

Relying solely of left "experts" is totally stupid. Keynesian economics should have been flushed out of the education establishment well before it became mainstream. Keynes' theories were Marxist and have produced market turmoil from the start. Like the "new" math, they sound smart only because they make sense to no one but those educated beyond their intellects. They rely on convoluted logic dissociated from reality. Consumers do not have any powers to influence inflation any more than their ability to influence unemployment.

What drives inflation are the double influence of unbacked, therefore creatable on demand, currencies and government unfunded spending policies. Both of which are under the control of politicians. If they taxed at the same level that they spend, they could not continue to get re-elected. If they had to deposit precious metals to back the dollars, they print they couldn't print freely. That is rightly called maintaining the value of our currency that the constitution demands.

We need to go back to backed currency and balanced budgets. There are no other methods by which politicians can be judged on the economy. All of the Keynesian debate about the economy is playing with words without meaning. And that is the only language spoken at the FED, D.C. and in the press.

I'm probably on the dovish end of the debate, so I want to agree with Tankus and Sahm, but it drives me nuts when doves trot out this argument that the 70s are just an N of 1 and we can't draw any lessons from it on combating inflation. If only there were perhaps other countries, who might have also had periods of high inflation that we could also use to guide us. The total inability to consider things that happened beyond America's shores is mind-boggling.